HMRC criminal investigations in 2022/23: An update

Locations

The year 2022/23 saw an evolution in HMRC's approach to criminal investigations, as articulated in a policy paper released in December 2021. Authored by George Gillham, Head of Contentious Tax, and Quinton Newcomb, Head of Commercial Crime, at Fieldfisher LLP, this update explores the nuanced changes in rhetoric and strategy employed by HMRC in tackling tax fraud.

Change in rhetoric and change in approach

In December 2021, HMRC released a policy paper outlining its stance on tackling tax fraud. In a succinct manner, the document delineated four key criteria guiding HMRC's decision to deploy its criminal investigation powers:

- Serious fraud - involving substantial losses or organised crime groups.

- Deterrence and equity - to send a strong deterrent message and assure the honest majority there is a level playing field.

- Insufficient civil powers - when HMRC's civil powers prove inadequate to unearth the truth or recover the tax at stake.

- Outcome-driven focus - HMRC's emphasis lies on achieving the right outcome for the UK, prioritising this over pursuing arbitrary targets for arrests and prosecutions.

Highlighting the societal importance of tackling tax evasion, we agree that it is crucial to focus on the most pernicious forms of it. Simultaneously, we recognise the pivotal role HMRC should play in targeting specific business sectors or customer groups where tax fraud is prevalent, fostering fairness in the tax system. Acknowledging HMRC's use of covert surveillance in a criminal context, we note the strict adherence to rigorous internal procedures required to authorise such surveillance efforts.

On the point about HMRC focusing on 'reaching the right outcome for the UK', we agree that this is the right approach to take. Criminal investigations are very expensive and time consuming, and they have an extremely serious impact upon those who are subject to them, so it’s only right that HMRC use them selectively and focus on the most harmful, complex and sophisticated frauds, and when there is a solid evidential basis for doing so.

Whilst tax fraud did not expressly feature in the Government's recently published Economic Crime Plan 2: 2023-2026, on the basis of, "the maturity of HMRC's existing response", it did include the following statement: "…tackling [tax fraud] remains an economic crime priority for Government as it is still one of the highest proceeds of crime generating public sector fraud risks. Robustly bearing down on evasion ensures individuals and businesses continue to believe there is fairness in the tax system. Many of the Plan’s actions will have positive consequences in tackling tax crimes".

The actions referred to that will assist HMRC in pursuing this Government priority include the announcement of a £400 million boost to the fight against economic crime over the next two financial years, in addition to the Economic Crime and Transparency Act 2023 ("the New Act"), which passed into law on 26 October 2023, which has brought with it important new law enforcement tools, which will be at the disposal of HMRC going forward.

Numbers and impacts

We have explained previously in posts on Fieldfisher Insights, and the Fieldfisher 'Tax Deductions' blog that there are a number of figures that Fieldfisher tracks that reveal the extent of HMRC's criminal investigations activity, and the extent of its success (or failure):

- search warrants executed by HMRC ("raids");

- decisions by the CPS to charge for tax offences ("decisions to prosecute");

- individuals prosecuted ("prosecutions"); and

- convictions for tax offences in the courts ("convictions").

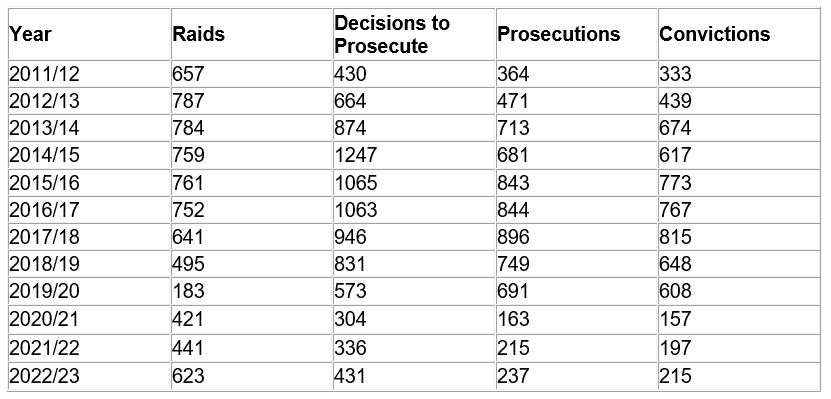

Over the last decade we have obtained, by way of requests under the Freedom of Information Act 2000, figures using these definitions (i.e. excluding tax credits offences) for all tax years from 2011/2012 to 2022/2023. Raids

Raids

Raids are up more than 40% in 2022/23. We think this is a result of HMRC fully resuming 'business as usual' enforcement activity after the pandemic, and starting to address the backlog of investigations which were delayed by the associated restrictions. It's also a very substantial investment, so in pursuing such activity, so in the case of those subject to raids, HMRC will consider that they may have committed the most serious forms of tax evasion. Raids take weeks or months meticulously to plan, involve the committing of very large amounts of human resource, and are followed by weeks and months of analysing the data yielded by the raid, not to mention legal challenges, which can be protracted and costly for the parties; so HMRC do not embark upon them lightly.

Decisions to prosecute

The number of decisions to prosecute has also jumped, likely reflecting the government's desire to take a tough line with businesses that illicitly exploited the Government's job assistance programs through the COVID pandemic.

The government's attention to 'get tough' is further evidenced by the publication of the policy paper by HM Revenue & Customs on 18 July 2023 proposing the doubling of maximum sentences from 7 to 14 years for a whole swathe of 'fraudulent evasion offences'. Of course, there is also the biggest stick of all, cheating the public revenue contrary to the common law, which carries two unusual features – in that it can be committed by failing to act, as well as by acting; and also it carries a maximum sentence of life imprisonment.

The New Act has brought with it two key changes to the law, which are likely to precipitate a further increase in prosecutions.

The first is to amend the decades-old principle of corporate criminal liability, so that it is easier to prosecute companies – with the actions of a senior manager being capable of giving rise to that liability, with the previous law in practice requiring evidence of criminality at Board-level.

The second is the introduction of the failure to prevent fraud offence, which will see a company liable if a person associated with it commits a specified fraud offence intending to benefit the company, or anyone else to whom the associated person provides services on behalf of the company.

Whilst HMRC has, for some time, had available to it the offence of failure to prevent tax evasion, and has faced criticism for not using it more readily, the broader offence will capture a broader range of fraudulent misconduct that HMRC encounter in their investigations, and the increasing Government emphasis on seeking to hold companies criminally accountable will surely translate in to more corporate prosecutions in time.

Prosecutions and convictions

Mirroring the increase in raids and decisions to prosecute, the number of prosecutions also rose in 2022/23. And, 90% of prosecutions resulted in a conviction, which is impressively high, and far higher than the rates seen in recent years for other UK law enforcement agencies, such as the Serious Fraud Office. HMRC and the CPS are to be commended for focusing their resources on bringing to trial high quality tax fraud cases with a realistic prospect of conviction.

What does this mean?

Because the chances of a decision to prosecute, prosecution, and conviction resulting from the raid are all extremely high, if a taxpayer is the subject of a raid by HMRC, they are in really serious trouble The taxpayer needs immediate, specialist support from lawyers with experience of HMRC raids, and dealing with serious criminal enforcement. For more on this see our Fact Sheet.

There's a second aspect to this, which has gained greater focus over the past few years. That is the mental health impact of being the subject of a raid, whether for an individual suspect, or for employees who work for a corporate suspect. A raid is a deeply, deeply, unpleasant experience.

For many, especially regulated professionals, it is their first contact with the sharp end of law enforcement. Individuals subjected to a raid commonly feel that their home has been violated. Their family will commonly be asking them (often fairly forcefully) what they have done for this to happen. If employed, the individual invariably has to undergo the humiliation of informing their employers that they have been arrested and their home searched. Often, their employer will have their offices searched too. Because tax fraud is a dishonesty offence, regulated professionals commonly need to inform their regulator that they have been arrested on suspicion of committing the offence. Often, as a result, the regulator suspends that individual's licence. Often as a result of that suspension, the individual will be suspended without pay, or sacked, by their employers. The net result is that even someone ultimately adjudged not guilty of tax fraud in a court of law can lose their family, home, and career. Even the risk of these losses occurring can lead to dark thoughts, and the uncomfortable truth is that suicidal ideation is common among those arrested on suspicion of tax fraud. Anecdotally, some try to commit suicide; and some succeed. It is for this reason that we ensure that we support our clients in getting professional mental health support to help them cope, and we never assume that they are coping emotionally with the experience.

Corporate clients too are increasingly seeking to address the mental health implications of such corporate crises. By way of example, ethics and compliance lawyers have worked closely with psychologists in exploring with clients the fostering of an environment of psychological safety for whistle-blowers - whose reports may be triggered by, or the trigger for, law enforcement activity. Seeking to foster a positive corporate culture, with strong support for those who report wrongdoing, can provide companies with an exponentially greater chance of early internal reports of tax fraud, or other wrongdoing, and, in turn, a much better chance of being able to control the process arising from such incidents, and, in many cases, avoid the risk of a raid altogether. It is self-evidently better for a company to receive a report of wrongdoing internally, and have the opportunity to investigate it before making an informed decision as to whether it is necessary to take steps against individuals and/or self-refer to the authorities, than by being forced onto the back foot by a raid that they never saw coming. That said, it is impossible to negate the risk of raids, and so companies should ensure that their teams receive regular dawn raid training, and that clear raid protocols are set out for their teams, and refreshed on a regular basis. HMRC are not the only agency with the power to raid, and Fieldfisher have specialists who can come together to provide training covering all major law enforcement risks, including police and National Crime Agency, Competition and Markets Authority, Serious Fraud Office, and Financial Conduct Authority raids.

And, there's a third aspect. Being the subject of a raid is not the only way to get yourself prosecuted. You can also be prosecuted for making a false statement during a compliance check. The recent successful prosecution of Bernie Ecclestone for lying during a COP9 investigation – thus committing fraud by false representation – not only involved his receiving a suspended prison sentence but paying swingeing penalties in relation to an incomplete disclosure of offshore income and assets. So, our recommendation is that no-one should attend any COP9 meeting with HMRC, or sign any statement of full disclosure, without taking specialist legal advice. It could save you hundreds of millions of pounds, as well as your liberty and life. It is for this reason that Fieldfisher has built a cross-disciplinary platform with specialist tax enforcement lawyers, from former Tax Inspectors to those who have prosecuted HMRC cases.

A version of this article was published by Tax Journal.