Locations

Which firms are in scope?

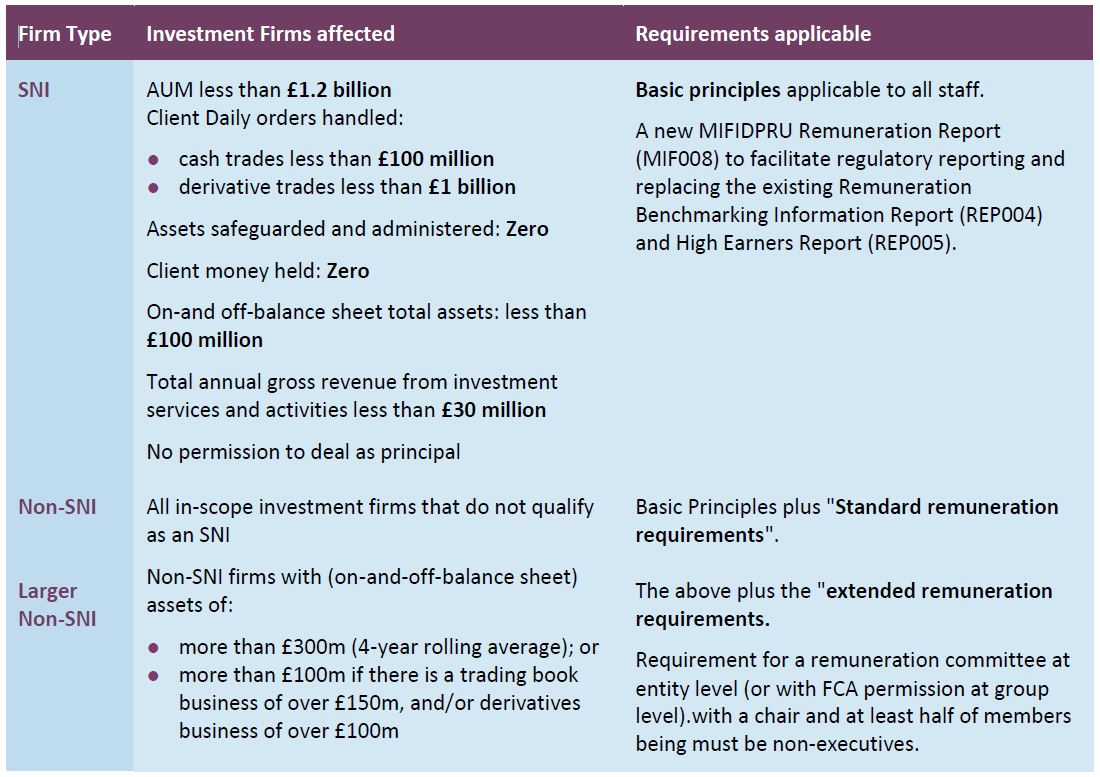

The IFPR will apply to all FCA regulated investment firms (but not dual-regulated firms) including BIPRU, IFPRU (full scope’, ‘limited activity' and ‘limited licence’); and 'exempt-CAD' firms. It affects also specialist commodities derivatives investment firms that benefit from the current exemptions on capital requirements and large exposures. Also affected are the regulated and unregulated holding companies of groups that contain such an investment firm.The IFPR Remuneration Code will apply to all investment firms but not all of the rules will apply to every firm. Essentially, for the purposes of this regime firms are divided into three tiers:

CPMI firms (i.e. those that undertake collective portfolio management as well as a MiFID investment business) will have to apply this code alongside whichever of the codes (the AIFMD Remuneration Code (SYSC 19B)) or the UCITS Remuneration Code (SYSC 19E)) may apply to them - with less flexibility about how to do this than has existed up to now.

The Basic principles applicable to all staff include:

● requirements for a remuneration policy complying with the Code and policies to be in line with the business strategy, objectives and long term interests of the firm including the firm's risk appetite, strategy and ESG risk factors;

● requirements to identify how fixed and variable remuneration is to be balanced; and

● new rules concerning the treatment of carried interest and coinvestment where a loan is provided (which will be particularly applicable to CPMI firms).

These are principles-based and offer SNI firms a degree of discretion.

The "Standard remuneration requirements" which apply to all Non-SNIs are more prescriptive. They include requirements for:

● Annual identification of MRTs (and there is new guidance on their identification and a new FCA approved template which firms can use to record this);

● setting appropriate ratios between fixed and variable remuneration (but not subject to a regulatory cap);

● detailed requirements on performance assessment and risk adjustment (ex-ante and ex-post – for which there is now amended guidance in FG21/5); and

● rules limiting guaranteed variable remuneration, retention rewards, buy-out awards and severance pay.

The "extended remuneration requirements" include requirements in relation to MRTs for:

● the deferral of variable remuneration, (40% of variable remuneration to be deferred for at least three years and 60% to be deferred where it is a particularly high amount) and vesting (not faster than pro rata);

● requirements for part (50%) of variable remuneration to be to be paid out in shares of the firm or instruments providing equivalent ownership interests or non-cash ;

● retention periods in relation to those instruments;

● requirements relating to discretionary pension benefits for MRTs, including requirement for a minimum period of holding pension benefits in the form of shares or non-cash instruments (including those settled in cash) which reflect the instruments of the portfolios managed.

In an approach similar to – but not the same as – the existing rules, only MRTs earning variable remuneration exceeding £167,000 (i.e., no maximum total remuneration) and whose variable remuneration which is in excess of one third (1/3) of total remuneration will be subject to the rules on:

● deferral of a portion of variable remuneration;

● pay-out of a portion of variable remuneration in shares, instruments or alternative arrangements; and

● the holding and retention periods for discretionary pension benefits when an MRT leaves the firm.

What is the impact of this?

For firms already applying IFPRU (SYSC 19A) or BIPRU (SYSC 19C) Remuneration Codes, this may be evolution rather than revolution. But for exempt CAD firms becoming non-SNI firms some of the requirements may affect profoundly how they go about rewarding their most important staff.In particular firms that for the first time are having to deal with the requirement to pay part of the variable remuneration in the form of shares or similar instruments there may be substantial hurdles to overcome to do this in a way that does not upset existing shareholder arrangements and is not disastrous for employees from a tax viewpoint. Often a creative approach may be needed perhaps:

● to create a new class of share that may be used for this purpose;

● to put in place trust or nominee arrangements; or

● to design a "phantom share" arrangement that is regarded as creating an equivalent "eligible instrument".

Where a firm is unable to issue eligible instruments share, the firm may apply to the FCA for a modification to permit the firm to use alternative arrangements but this is likely to be available only in certain limited circumstances (e.g. because it is an LLP not a company limited by shares).

What do I need to do?

Firms need to:● confirm who are to be regarded as their MRTs having regard to the amended guidance;

● review their employee remuneration arrangements, especially for MRTs. This is likely to require amendments to firm's Compliance Handbook, an Employee Handbook if the firm has one and may require changes to employment contracts;

● review any relevant pension arrangements;

● if the firm has MRTs who are subject to the requirement to pay part of the variable remuneration in the form of shares or similar instruments then arrangements need to be made for the issue of suitable instruments. This may require corporate advice and tax advice.

The FCA's Remuneration Policy Statement template provides a useful template for considering the rules as does its template for recording material risk takers.

When do I need to do this?

There is little time now for firms prepare for these new rules. The new rules apply to "performance periods" beginning on or after 1 January 2022, so potentially they apply to firms that judge annual performance on a calendar year basis from this date, although firms that use different performance periods (e.g. half yearly starting on 1 April) may have a little more time for elements of this.The FCA has also announced that it will be sending out a questionnaire to firms in November asking for the information they need to update their systems and reporting schedules in preparation for the new regulation.

How can we help?

We have found that many of our clients require assistance in interpreting and applying the new rules, particularly in understanding issues such as:● the calculation of on-balance sheet and off-balance sheet assets for the purpose of working out which tier of the regime applies;

● defining what counts as fixed remuneration and variable remuneration, including in marginal cases (such as profit shares where the firm is an LLP or carried interest/coinvestment arrangements);

● application of the concepts of "vesting", "malus" and "clawback" and how this is to be put into service contracts;

● the types of arrangements which may be used to satisfy the requirement that 50% of variable remuneration is awarded by the issuance of "eligible instruments” as required by SYSC 19G.6.19R to SYSC 19G.6.21G (Shares, instruments and alternative arrangements) and how these may be implemented in a particular commercial setting.

Combining our expertise in financial services regulation with our leading position in relation to the design of employee rewards arrangements, we are well placed to assist in the design of reward structures whether these involve shares in the company, and Employee Ownership Trust, carried interest vehicles or "phantom share schemes" and to assist firms in ensuring compliance with the detail of these new rules.

Contacts

Nicholas ThompsellDuncan Black

Mark Gearing

Simon Lafferty

Steven Burrows

Monique Marino