The FCA Proposals for a Duty of Customer Care

Locations

Caveat Venditor: The New Consumer Duty:

It looks as if firms will be required by 30 April 2023 to comply with the FCA's new Consumer Duty. This is not just another rule change. It brings about a radical change in how firms treat their retail customers. Firms have until 15 February 2022 to comment on the proposed new requirements. Firms that deal with retail customers should be considering in detail the implications for their business.

The Consumer Duty

The Consumer Duty is coming.

The Financial Conduct Authority (FCA) has been proposing a new consumer duty for some time and the proposal was the subject of the FCA's consultation paper CP21/13: A new Consumer Duty (fca.org.uk), published in May 2021. The FCA's second Consultation Paper (CP 21/36), published in December 2021 solidifies the FCA's thinking on this matter and sets out draft rules and guidance. With the publication of this second consultation paper, it now seems inevitable that something like the proposal set out in that paper will find their way into regulation.

What is the Consumer Duty intended to do?

The Consumer Duty intends to require firms to:

- ask themselves what outcomes consumers should be able to expect from their products and services

- act to enable rather than hinder these outcomes

- assess the effectiveness of their actions.

The FCA expects the Consumer Duty to have radical effects - a step-change in regulation intended to change the way that firms think about the relationship with customers who are consumers.

The implications of the duty are wide-ranging. The FCA sees this becoming a cornerstone of its supervisory and enforcement approach. The duty has implications for product design, product marketing, the data that the FCA expects firms to collect, the handling and analysis of complaints and the Threshold Conditions that the FCA considers when authorising new business.

Of course the more radical the change, the less predictable its outcome.

Why is the FCA introducing this?

The FCA has good reasons for proposing the duty. It hopes that the duty provides a higher level of consumer protection through firms competing vigorously in the interests of consumers resulting in consumers making informed choices and getting products and services that are fit for purpose, that provide fair value and that they understand their use.

In the FCA's view, this is not always happening now: firms are not consistently and sufficiently prioritising good consumer outcomes, causing consumer harm and eroding consumer trust.

The FCA has in mind specific practices that work against consumers (or at least some consumers).

Examples of poor practice the Duty intends to end

|

To which firms does the FCA propose applying the Consumer Duty?

Any firm providing financial services or payment services (including any electronic money issuer) that deals with retail clients needs to start considering in detail the implications of this for its business.

For the most part, as mooted in the FCA's original proposal, that the duty is to apply to financial services and products provided to ‘retail clients’, as opposed to the narrower category of ‘consumers’ (broadly individuals acting for purposes outside their business or profession) to which other consumer protection legislation applies. Retail clients include clients that are not professional clients or eligible counterparties.

However, following its first consultation, the FCA has acknowledged that this definition (applicable to investment business) may not be appropriate in some other sectors such as insurance or mortgage businesses and so the application rules are now nuanced to apply appropriately according to different types of business.

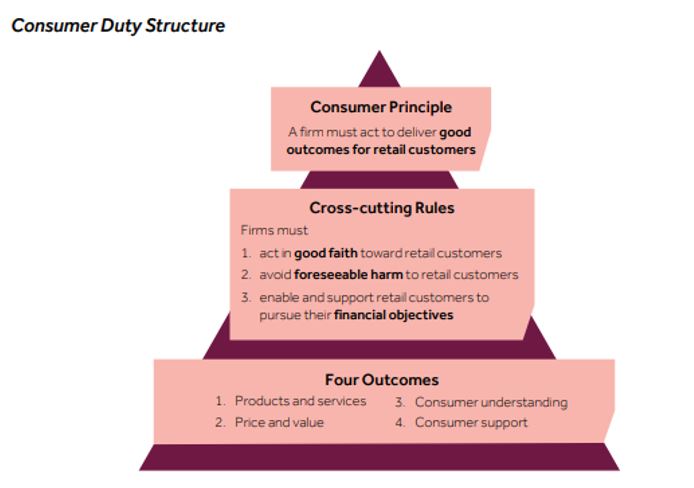

What is the proposed structure of the Consumer Duty?

The Consumer Duty proposes three elements, considered further below:

• A Consumer Principle

• ‘Cross‑cutting Rules’ which develop the FCA's overarching expectations for common themes that apply across all areas of firm conduct,

• The ‘Four Outcomes’: a suite of rules and guidance setting more detailed expectations for firm conduct for 4 specific outcomes representing the key elements of the firm‑consumer relationship., which would be added to the principles set out in the PRI section of the FCA's Handbook.

Diagram reproduced from CP21/36

The Consumer Principle

The FCA has settled on the following wording for the proposed Consumer Principle:

‘A firm must act to deliver good outcomes for retail clients’

The FCA sees this as reflecting the shift it wants to see with firms consistently focusing on consumer outcomes.

The Consumer Principle is not some toothless mission statement with no consequences. The FCA intends to add the principle to the list of principles within the PRIN section of the FCA Handbook and very often, when the FCA brings enforcement action, it bases it on non-compliance with one of these principles rather than the breach of a specific rule.

On first sight, the breadth of this principle looks alarming. It looks as though there is a breach of the principle whenever a consumer reasonably considers that he or she has not had a good outcome. This is not the intended effect. The FCA does not expect that consumers can or will be protected from all harm. It is not looking to impose an open-ended duty that goes beyond the scope of the firm’s ability to determine or influence consumer outcomes or protect consumers from all potential harms, or to remove the principle of consumer responsibility.

For example, the FCA acknowledges that a borrower whose house is repossessed, or an investor who loses money on an investment may feel they have not had a good outcome, but the firm may be considered to have acted in line with the Consumer Principle if the firm has acted reasonably to deliver good outcomes. The draft rules and guidance reflect this acknowledgement.

If this is the intended effect, one might ask why the word "reasonably" is not included within the draft principle. This is a point that firms might want to make in response to the consultation.

The Consumer Principle proposes to affect more than just firms dealing directly with retail clients. It would be applicable to firms who do not have a direct contractual relationship with a retail client, but who nonetheless are involved in the manufacture or supply of products and services to retail clients. This will add to any existing product governance rules, requirement for manufacturers and wholesale distributors to cooperate with those of the retail end of the market to ensure the appropriate design and targeting of products.

The Proposed Cross-Cutting Rules

The FCA proposes the following as "cross-cutting" rules

Firms must:

- Act in good faith towards retail customers. Described as a standard of conduct characterised by honesty, fair and open dealing and acting consistently with the reasonable expectations of retail customers.

- Avoid causing foreseeable harm to retail customers. Requires a firm to be both proactive and reactive in designing and marketing products and to take protection to mitigate the risk of actual or foreseeable harm.

- Enable and support retail customers to pursue their financial objectives. The rule applies differently for firms providing execution-only service or a non-advised service from that which provides advisory or discretionary services.

The Four Outcomes

The FCA proposes four outcomes and has provided new draft rules and guidance in respect of each of these. The four outcomes are:

- The Product and Services Outcome. This involves new requirements proposed to apply to manufacturers and distributors of products or services (and the line between the two may be blurry) to introduce new processes, testing and monitoring procedures to ensure that products are aligned to consumers' requirements and needs.

- The Price and Value Outcome. The FCA acknowledges that fair value is about more than just price, and it is not looking to impose price regulation, but it does focus on getting firms to ensure that the price of the products and services are proportionate to their value. As with many areas within the proposal, this is one where one needs to consider the wording of the draft rules and guidance in order to understand what is the import of these widely framed outcome objectives.

- The Customer Understanding Outcome. This requires communications tailored to the information needs of the target audience, and again will be one where the detail of the rules and guidance will be of prime importance. It proposes new requirements for testing, monitoring and adapting communications.

- The Customer Support Outcome. This proposes the customer support that firms who interact with retail customers provide and aligns to other rules that cover specific elements of the servicing of customers, such as the DISP rules on handling complaints. There is a focus on meeting the needs of retail customer, ensuring that they can use the product and do not face unreasonable barriers when they make requests to the firm, wish to amend or switch a product, transfer to a new provider, or wish to make a complaint or to cancel the contract. Again, there are new requirements on monitoring the outcomes that retail customers are experiencing.

In addition, but not labelled as an 'outcome' it is proposed to develop further rules of guidance about how firms are expected to deal with consumers who are considered to be vulnerable or in vulnerable circumstances.

Private Right of Action

The FCA has not yet decided whether it should propose it makes any element of these new requirements the subject of a 'private right of action' (PROA). This applies provisions within the Financial Services and Markets Act 2000 so that an individual who has suffered a loss through a firm's breach has a right to take legal action for damages from the firm. It is not proposing to do this initially, but is expecting to keep this under review, but this decision is the subject of consultation.

The FCA's proposal on this point seems to be sensible. Much of the proposed new regime is subject to nuance and guidance. It is surely correct that enforcement of this should be in the hands of the FCA and the Financial Ombudsman Service, rather than being left to individuals (perhaps egged on by claims management firms) to bring actions based on what may be an overzealous understanding of the intended scope of the Consumer Duty. Firms who are concerned to avoid the prospect of a PROA applying may wish to respond to the consultation to support this.

What do now?

The FCA expects firms to prepare for this based on the draft rules and guidance now available. It is proposing an implementation timetable, giving firms until 30 April 2023 to implement fully the Consumer Duty (although the FCA is still consulting about the timing).

Firms who deal with retail clients must read the latest consultation paper and think about the implications of this for their businesses. Compliance with the duty is likely to require some re-engineering processes for almost all firms involved in retail products or services, and for some may require some radical changes.

Firms should consider making representations about it if they have any concerns about the proposals and they should start thinking about what changes they need to make to comply with the new duties.If you would like any support in thinking about this, please contact your usual Fieldfisher contact or one of the following:

Nicholas Thompsell Nicholas Thompsell+44 330 460 6523 |

Duncan Black Duncan Black+44 330 460 6472 |

|

Simon Lafferty Simon Lafferty+44 330 460 6497 |

James Tinworth James Tinworth+44 330 460 6485 |

|

Dale Gabbert Dale Gabbert+44 330 460 6520 |

Kirstene Baillie Kirstene Baillie+44 330 460 6522 |