Locations

In China, an eligible applicant can apply for a Certificate of Chinese Fiscal Resident for free of charge under certain conditions in order to enjoy the treatments indicated in tax treaties entered into between China and foreign countries (including the tax arrangements or agreements entered into with Hong Kong, Macao and Taiwan).

For instance, under Belgian tax law, interest paid by a Belgian company are in principle subject to with holding tax (“WHT”). The ordinary WHT rate is set at 30%. Pursuant the Double Tax Treaty between China and Belgium, this amount can be reduced to 10%. However, to be fully valid, the reduction must meet certain formalities including the filing reduction application form. The Certificate of Chinese Fiscal Resident may be required.

In this article, I will briefly discuss how to apply for a Certificate of Chinese Fiscal Resident so that applicant may benefit from the applicable tax treaties.

Who is eligible to apply

• Individuals

Individual who has domicile in China, and Individual who has no domicile in China but has resided in China for at least 183 days in a tax year may eligible to apply.

According to Individual Income Tax Law of the People’s Republic of China (“IIT law”), Individuals who have a domicile in China or individuals who do not have a domicile in China but have resided in China for an aggregate of 183 days or more within a single tax year shall be deemed as resident individuals from Chinese tax law perspective.

A tax year begins on January 1 and ends on December 31 of a calendar year.

According to the relevant IIT laws and regulations, having a domicile in China means individual who habitually residing in China because of his or her permanent residence, family or economic interests.

• Enterprises

Enterprises legally established in China or established in accordance with the laws of foreign countries (regions) but with actual management office in China may eligible to apply.

According to Enterprise Income Tax Law of the People’s Republic of China (“EIT law”), the resident enterprises refers to Enterprises that are established in China, or Enterprises that established outside China but its actual management office is in China.

Where to file the application

An applicant shall apply to the tax authority at the county level which is in charge of the applicant's income tax (the "competent tax authority") for issuing a Fiscal Resident Certificate.

Domestic and overseas branches of a Chinese resident enterprise shall file an application through their head office in China with the competent tax authority of such head office.

With regard to a partnership, however, its Chinese resident partner shall act as the applicant to file an application with the competent tax authority of such partner.

What materials shall be submitted

In general, the materials below shall be required to file the application.

1. an application for a Certificate of Chinese Fiscal Resident

2. supporting documents relating to the income that may enjoy the tax treaty treatments, including contracts, agreements, resolutions made by the board of directors or board of shareholders, and the relevant payment documents

3. for Individual who has domicile in China, supporting documents such as the applicant’s identify information and domicile information would be required

4. for Individual who has no domicile in China but has resided in China for at least 183 days in a tax year, supporting documents demonstrating his or her actual residence status in China such as record of his or her exit and entry of China would be required

5. supporting documents demonstration registration status of the head office and branch would be required when a domestic or foreign branch files the application through its head office

6. registration status of the partnership would be required when a Chinese resident partner of a partnership files the application as an applicant

The relevant documents shall be filled out or submitted in Chinese. Chinese translations shall be provided where the original of the relevant materials are in a foreign language.

Additional materials may be required if the tax authority finds the case complex and unable to determine based on the existing documents.

How long it takes

Usually it takes 10 business days from date that the tax authority accepts the application form and all relevant materials to issue the certification; It takes 20 business days to issue the certification if the case is complex. In practice, however, the progress is fairly quick. It may take less 10 days to issue the certificate.

For instance, Shandong Provincial Tax Service, State Taxation Administration promised that 3 business days for standard applications, and 7 business days for complex applications that need to be reviewed by a higher level of tax authority.

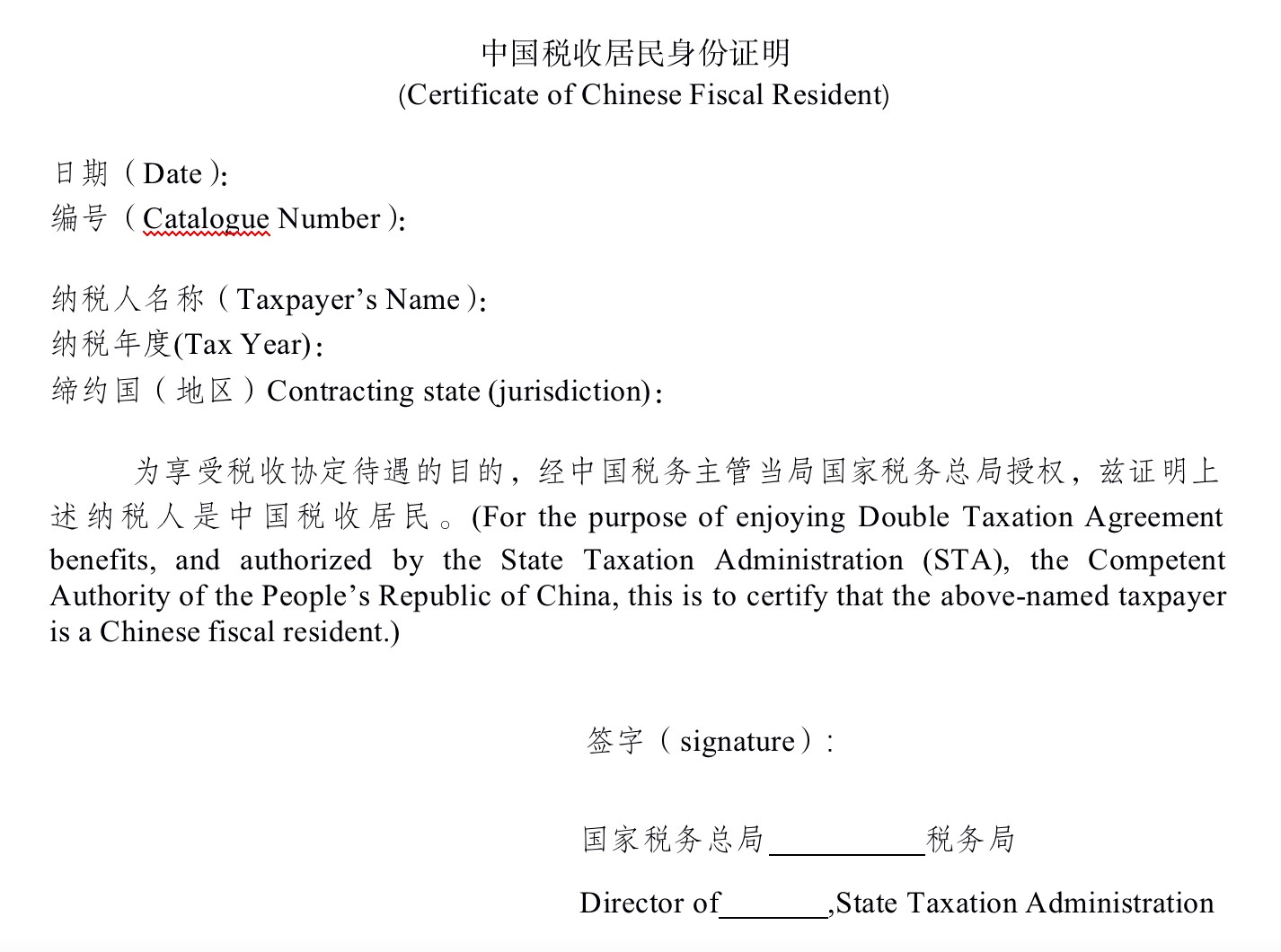

Format of the Certificate

A standard form of a Certificate of Chinese Fiscal Resident shows below.

However, if the competent tax authority of the other Contracting State has specific requirements on the format of certificate of fiscal resident, the applicant shall submit relevant instructions in written and the required format, and the competent tax authority in China may issue the certificate according to the special requirements.

Other issues that worth to mention

• An electronic signature is acceptable

An application for an electronic signature that meets the conditions stipulated in the electronic signature law has the same legal effect as a written signature or seal.

• Taxpayer’s Identification Number

For Individual who has no domicile in China but has resided in China for at least 183 days in a tax year, the Taxpayer’s Identification Number in China may be requested.

• Notarization is not mandatory

In general, the notarization is not mandatory for submitting the supporting documents unless the competent tax authority requires.

Fieldfisher’s tax teams in China and Europe are available to assist individuals and businesses with any Cross-board tax issues.

NOTE: The information in this article shall not be deemed to be, or serve as, legal advice.