Locations

A foreign partnership, without an establishment in China, and its overseas property transfers shall not be subject to Chinese tax in general.

However, an indirect transfer shall be re-characterised as a direct transfer of China Taxable Property[1], and subject to Chinese tax. The latter would only apply provided that the transfer is conducted by a foreign partnership (through arrangements that lack reasonable commercial purposes), and the said foreign partnership avoids Enterprise Income Tax (“EIT”) – hence, liability through the means of the transfer[2].

Under the same announcement above, there are three type of transactions which would be exempt from the income from the indirect transfer, under certain conditions: Intra-group Re-organization; Public Securities Market Transaction; and Applicable Tax Treaties.

This article addresses how to apply one of the “Safe Harbour” rules, which is how the income from the indirect transfer may result in being exempt from EIT (in China), in accordance with the applicable tax treaties, when and if the indirect transfer has been conducted as a direct transfer.

About the Facts[3]

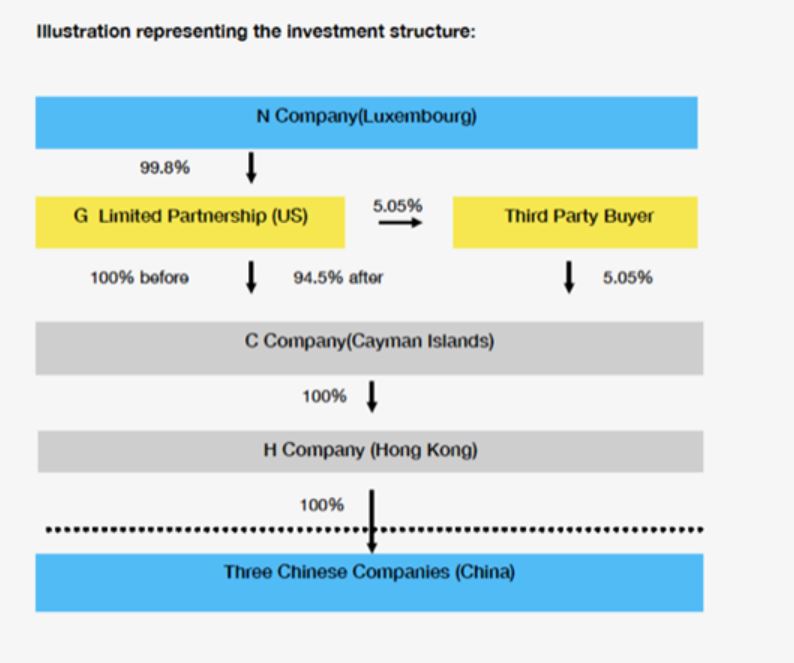

N was registered in Luxemburg as a private company with limited liability. It is a limited partner, which holds 99.8% of the shares of G. G was registered in the United States as a domestic limited partnership, which holds 100% shares of C. C was registered in the Cayman Islands, which holds 100% of the shares of H. H was registered in Hong Kong. N, G, C, and H (as holding companies) invested in three Chinese resident companies, in China.

In 2018, 5.05% of the shares of the three Chinese companies were transferred to a third party – such was done indirectly by G, who transferred 5.05% of its shares of C to the third party.

After the transaction, G claimed that the income generated from the indirect transfer of its assets, by non-resident enterprises, shall not be subject to the enterprise income tax in China as based on self-examination, Article 5(2) of Announcement No.7, where such may apply to this transaction. If the latter applies, G shall be exempt from the Enterprises Income Tax (EIT), purporting to this transaction.

Whether the income generated from the transaction between G and the third party could be exempt from EIT, in China, by applying one of the “Safe Harbour” rules under Announcement No.7 - which states the circumstances under which a non-resident enterprise, which holds and transfers its China Taxable Property (according to the applicable tax treaty), and the income generated from the said transaction would be exempt from EIT, in China.

The Tax Authority’s Analysis

The in-charge tax authorities did not grant G’s application as the tax authorities determined that the “Safe Harbour” rule under Article 5(2) of Announcement No.7 does not apply to this case. Such was due to the fact that the transaction fell short of the conditions imposed by the tax treaties, for two reasons: (1) G is not a US resident for tax purposes, therefore the US-China tax treaty does not apply; and (2) G was registered in the United States, and was not a resident in Luxemburg, therefore, there are no special provisions to address the “pass through” issue in the tax treaty between China and Luxemburg, which does not apply to this transaction either.

Under the law in China, unless otherwise stipulated by tax treaties, the income of the foreign partnership (which is taxable in China), may be entitled to a claim through the tax treaty benefits - such would be possible only when the foreign partnership is a resident of the other Contracting State. In other words, in this case, G (as a partnership) is unable to claim the tax treaty benefits, provided that it does not subject itself to pay tax under the domestic law in the United States.

From the United States tax law perspective:

Form 1065[4] shows that G is a domestic limited partnership registered in the United States. According to 26 U.S. Code § 701, “A partnership as such shall not be subject to the income tax imposed by this chapter. Persons carrying on business as partners shall be liable for income tax only in their separate or individual capacities.” Thus, in this case, G (as a partnership), is not a US resident for tax purposes.

The US-China tax treaty provisions do not stipulate that if, under the domestic law of the other Contracting State, the income derived by the partnership is deemed as income of the partner, then the partner may be entitled to claim tax treaty benefits - with respect to the part of the income which it drives from the partnership.

Hence, since G is not a US resident for tax purposes, no special rule can be applied here, either. The tax treaty benefits under Article 5(2) of Announcement No. 11[5] do not apply.

From the Luxemburg tax law perspective

N was registered (still existing) in Luxemburg, in 2012, as a private company with limited liability. Its actual management institution is located in Luxemburg, and its operation management was, and is, managed by the Board of Directors and Management in Luxemburg. Meanwhile, N was registered as a resident for tax purposes, and filed for its annual enterprise income tax return in Luxemburg.

N was a limited partner of G - which was holding and transferred the shares of three Chinese resident companies to the third party, indirectly. The tax treaty between China and Luxemburg does not apply to the income generated from this transaction, where G is the equity transferor.

The latter is due to the fact that G was registered in the United States, and was not a resident in Luxemburg. Unlike the tax treaty between China and France, there are no special provisions to address the “pass through” issue in the tax treaty between China and Luxemburg.

Therefore, both G and N were unable to claim tax treaty benefits based on Article 5(2) of Announcement No.7.

Key take-away points:

How to prove the foreign partnership’s identity from a tax perspective?

In practice, one of the key issues is proving the foreign partnership’s tax identity.

The Tax Resident Certificate submitted by the partnership (which is issued by the tax authority of the other Contracting State), shall be able to prove that the partnership (under the laws of the other Contracting State), is liable to tax therein by reason of his domicile, residence, place of incorporation, place of management, or any other criterion of similar nature[6].

However, the in-charge tax authority would not grant the said application even if the entity provides the Tax Resident Certificate issued by the tax authority of the other Contracting State, only for tax purpose, if it cannot prove that the partnership is paying tax in the other Contracting States.

What is the resulting tax consequence once the “Safe Harbour” rule, under Article 5 of Announcement No. 7, does not apply?

Under the Enterprise Income Tax Law, non-resident enterprises without an establishment in China, or with an establishment in China, whose income has no actual connection with the establishment, are subject to Chinese EIT - only on China-sourced income.

Once an indirect transfer is found to be lacking reasonable commercial purpose and no safe harbor applies, the indirect transfer will be re-characterised. As a result of such, the gain from an indirect transfer of equity interests in Chinese resident enterprises will be treated as China-sourced income, and will be subject to 10% withholding tax.

One open question, that is likely to be debated, is whether the elements of “Safe Harbour” would still be of relevance when assessing reasonable commercial purpose.

What’s the withholding obligation for offshore buyers and sellers?

Under Article 8 of Announcement No. 7, the payor has a withholding obligation on indirect transfers of equity interests, in Chinese resident enterprises. However, it fails to distinguish between a payor that is a resident enterprise and a non-resident enterprise.

The key issue is that offshore buyers and sellers, in most instances, are unable or not in a position to determine whether the indirect transfer is taxable in China - especially within the time limits imposed, and when the tax authority has no obligation to make a decision on the related taxability.

Therefore, a buyer who agrees in good faith with the seller, that a transaction has reasonable commercial purpose and decides to not withhold taxes; may still operate under the threat that the transaction could be re-characterised at any time during the next 10 years - which is the statute of limitation imposed upon transactions lacking reasonable commercial purpose.

Should the parties involved in the indirect transfer report the transaction to the in-charge tax authority?

Under the law in China, it is not mandatory for one to report any of the transactions related to the indirect transfer. However, the tax authority encourages the parties involved in the indirect transfer to report the transaction - as it becomes a big challenge for the tax authority to notice the transaction.

Therefore, the policy for both offshore buyers and sellers of an indirect transfer, and the underlying Chinese enterprises, may (although, not mandatory) voluntarily report the transfer by submitting a standard set of documents to the in-charge tax authority. Such is bound to make the process a more “friendly” one for all of the parties involved.

For instance, if the offshore buyer reports the transaction within 30 days from the date when the equity transfer contract/agreement, has been signed, then a potential exemption from/or a reduction in future penalties for any failure to properly fulfill the withholding obligation on the transfer may be secured.

However, it empowers the in-charge tax authorities to request various documents from the buyer and the seller of an indirect transfer, as well as from the underlying Chinese resident enterprises. The documents subject to request have a broad and unclear coverage, and include all decision-making and “implementation processes” information, for the whole arrangement relating to the indirect transfer.

Conclusion

Announcement No.7 has a significant impact on cross-border transactions and intra-group re-organisations involving China. The disputes concerning the indirect transfer of equity interests in Chinese resident enterprises have become a major issue in the recent years.

As such, whether the tax treaty can be applied to a foreign partnership is a highly complicated issue in China. Announcement No.11 clearly states that the Enterprise Income Tax Law in China is applicable to a foreign partnership, and that the tax treaty may apply as well. Thus, it is essential to determine whether the foreign partnership would be successful in claiming tax treaty benefits.

In practice, it is a tough decision to make for offshore buyers and sellers with their indirect transaction overseas - especially considering the fact that the in-charge tax authority has no obligation to issue a formal decision on the taxability of the transaction.

When the in-charge tax authority assesses tax liability, they tend to consider various determining factors when doing such, especially as cross-border and domestic tax law will often be involved. Hence, it is important to get international tax professionals’ assistance on the disputes/issues, to access their tax liability knowledge, in order to ensure that one is fully in compliance with the applicable laws.

* Special thanks to Ms. Bianca-Maria Durac who has helped by proofreading this article.

Please kindly note that this article does not constitute, nor shall it be considered to be legal advice in any way, it may be subject to change if the law has been issued, revised and/or abolished.

About Author:

Xiaoli Shi, a tax partner in Fieldfisher’s Shanghai Office (China)

[1] In this article, “China Taxable Property” refers to equity interests in Chinese resident enterprises.

[2] See Announcement of the State Administration of Taxation on Several Issues of Enterprise Income Tax on Income Generating from Indirect Transfers of Property by Non-resident Enterprises (SAT Announcement [2015] No.7, effective date: 3 Feburary 2015)) (“Announcement No.7”)

[3] The fact of case refers to 《税收协定执行案例集》(Case Study of Tax Treaties ),国家税务总局国际税务司 编著,(Written by State Tax Administration International Tax Department), 中国税务出版社(2019版)(China Taxation Publishing House)(2019 version) 第13-17页 (Page of 13 to 17)

[4] See https://www.irs.gov/instructions/i1065 (latest visit on 26 May 2021) Form 1065 is an information return used to report the income, gains, losses, deductions, credits, and other information from the operation of a partnership. A partnership doesn't pay tax on its income but passes through any profits or losses to its partners. Partners must include partnership items on their tax or information returns. However, one exception may be worth to point out which is, in the US Tax Code, the so-called “check the box” rule. It permits a US taxpayer to choose whether an entity is to be regarded as transparent or not for US tax purposes, regardless of the actuality. If the partnership choose to be regarded as opaquer for US tax purposes when it files its tax return. G’s tax identity may have impact on this tax treatment.

[5] Announcement [2018] No. 11 refers to Announcement of the State Administration of Taxation on Several Issues Concerning the Implementation of Tax Treaties, effective date: 9 February 2018

[6] See Announcement of the State Administration of Taxation on Several Issues Concerning the Implementation of Tax Treaties (Announcement of the State Administration of Taxation [2018] No.11 effective date: 9 February 2018) Article 5 (2))